Issue #5 - The Future of Manufacturing

Welcome to Issue #5. This issue focuses on lessons learned to invest in B2B hardware-as-a-service companies, computer vision in the shopfloor, selling to industrial mid-sized companies and an update of my industrial landscape among others.

I hope you enjoy reading it. If you do, any feedback, shares or links are much appreciated 🙏

Disclaimer: thoughts and opinions expressed in the newsletter are my own.

What I enjoyed reading

💰 Dealroom published a detailed report about European Venture Capital in 2017. There is one very interesting slide where they look at the number of investments by industry and compare the entire European VC market with rounds by "Europe’s top 30 investment firms" (Slide 21). If you look at the chart, it's noticeable that there is a big gap in manufacturing - it looks like Europe's top investment firms (Dealroom definition) have been very bearish about this industry last year since the number of investments is much lower compared to the entire European VC market.

{kind=link}

🤖 We're very bullish about hardware-as-a-service companies here at Point Nine and it's great learning more about it every day and working together with the founders. Rodrigo just shared a post where he talks about some lessons learned to invest in these B2B hardware-as-a-service companies. TL;DR: it's tough but it can be very defensible and you can still have software-like margins :)

🧐 Andy Bane, CEO of Element Analtyics, made an interesting observation a few weeks ago. Gartner, one of the world’s leading IT analyst firm, is increasingly focused on industrial analytics and has published several reports dedicated to this topic. In his view: "when a firm like Gartner starts tracking a sector, we believe it often means there are opportunities".

🤓 Product planning for enterprise products is very different compared to consumer products. One of the challenges is that the user and the buyer are often not the same person. John Dawes who has been leading enterprise product teams for over 20 years, explains in his blog post that you should also listen to the buyer, focus on demonstrating value and not just a great UX and partner with customers on objectives.

🎙️ There is no doubt that the industrial sector is a slow-moving industry (at least I don't have any doubts). However, that doesn't mean that founders can afford to be "slow" as well. Here is a very interesting interview with the CEO of Veeva where he explains that in the first year they only had a quarterly plan because at that stage it's irrelevant what will be in 12 months e.g. they could be out of business then already. Even though they are in healthcare, I think the same applies to manufacturing.

About industrial Startups and Companies

💸 Drishti - which calls itself the "Google for actions" just raised a $10M round led by Emergence with participation from existing investors a16z and Benhamou Global Ventures. The company founded by tech-veterans is using computer vision to recognize and record human actions on the factory floor. This means that they are able to measure assembly-line human labor productivity and efficiency at the factory floor.

🤑 The connected worker platform Parsable received $40M to reduce paper and bring more tablets and smartphones into the shopfloor together with its platform. This brings its total funding to $68M. The company has now 30,000 registered users on the platform, would be very interesting to know how many of them are "active users".

🚘 In the seed stage, Project A Ventures and Vito Ventures are adding another industrial startup to their portfolio called Artisense. In total, they raised $4M from the two German funds. The company is building an accurate and efficient solution for AI-based computer vision for autonomous vehicles and robotics and has offices in Munich and Palo Alto. I heard other European funds have also been quite active in the space but these investments haven't been disclosed :-)

Additional thoughts on recent development

Selling to industrial mid-sized companies ("Mittelstand")

There is a significant amount of founders who tell me that they are going after industrial mid-sized companies ("German Mittelstand") instead of enterprises because:

i) they have faster and less complex sales cycles

ii) they can talk directly to decision-makers, i.e. c-level, founder, MD

iii) they can still pay a good ACV

However, I have seen close to zero successful examples that this works at the early stage. Here is my take why:

i) the economy is in very good shape at the moment. The order books of these mid-sized companies are full for the next 12-18 months. There is no strong urgency in cost reduction but rather e.g. how to get the raw materials in time

ii) their biggest problem is the lack of talent, this is where they really spend a lot of time on

iii) they often don't know what kind of digital solutions they are looking for and need education which slows down the sales process, so a healthy ratio of sales effort and sales cycles vs. ACV is tough

There are counterexamples for sure and I'm happy to hear any successful examples and anecdotes.

Industrial Landscape

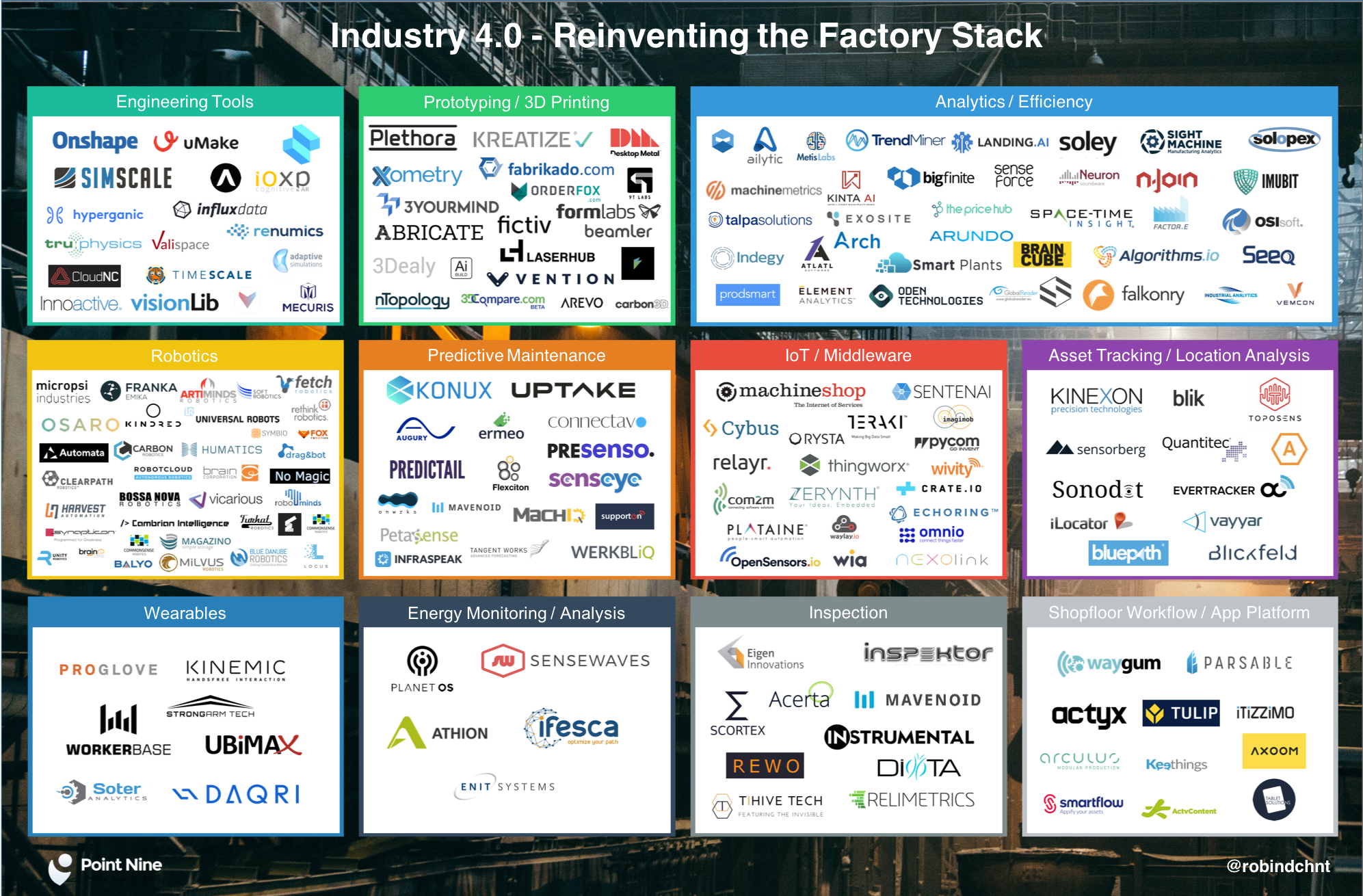

It took me quite some time but I did a big update on my industrial landscape and added more than 30 companies to it. The biggest increase has been in Robotics, Analytics / Efficiency, and Predictive Maintenance. There are now ca. 200 companies in the landscape (see below).

{kind=link}

Thanks to everybody for supporting this newsletter and for sending me interesting links. As always, any input, shares, and feedback are always warmly welcome.

Robin

P.S. I will be in Munich mid-June, let me know if you want to meet.