Issue #54 - The Future of Manufacturing

Topics this time: software-defined hardware companies, financing solutions for Capex-heavy businesses, an outlook for AI in 2027, new funding rounds in Q2 2025.

Welcome to Issue #54

I'm spending much more time again with entrepreneurs and operators across different manufacturing domains now that I’ve joined GC. It's a lot of fun. To spark a discussion here, you can find below a short summary of topics and thoughts that interest me - happy to hear your view on these:

Robotics time-to-value keeps shrinking: it's visible if you go to any robotics hackathon (we did one in Zurich) and spend time with builders in the space. It still blows my mind that people without robotics background can build robotics MVPs within 48h. Various initiatives are doing a great job at enabling a robotics grassroots community with software and cheap hardware such as the Huggingface SO-100 robotics arm

The race to own the production floor: Modern manufacturing software companies are often starting from point solutions like quality inspection, safety analysis or process analytics. There is a race to become the system of record for the Head of Production longterm. On top of this, there are a few new entrants trying to build a modern MES from the ground up. Time will tell which is the winning approach here, it’s an exciting topic to follow where several players can become large

European defence is attracting top talent: a wave of operators and engineers is moving into European defence startups, where hardware meets software in the toughest possible setting. Because GTM hurdles are very high, I expect a significant number of these builders to pivot later or join larger hardware–software scale-ups. Notably, some European operators are even relocating home from the US to build here

Europe is poised for inorganic growth: Full-stack modern hardware companies are beginning to acquire innovative SMBs: faster product extensions, cross-border sales channels, certification speed-ups are some of the reasons. In the current environment, investors are fine to finance these acquisitions. As more of these scaled hardware–software players emerge, I expect stronger M&A momentum to build here in Europe

Enjoy reading.

Robin

PS: I’m very excited to see some of my private portfolio companies announcing fresh financing rounds: Rivan £10M led by Plural and Sensmore $7M led by P9 Capital and Remberg €15M led by Acton Capital. Let’s go!

Got a friend or colleague interested in manufacturing? Help me spread the word by sharing the newsletter if you like it!

I. Frontier of Manufacturing

🎢 The amusement park for engineers

This article gives you a rare inside tour of Anduril’s R&D efforts: small cross-functional squads own a product end-to-end, prototype in days, test in the desert the same week, and feed data straight back into manufacturing. Author Adnan Esmail calls it an “amusement park for engineers” where welders, AI engineers and aero designers share the same hangar. The piece makes a convincing case that vertically-integrated, test-anywhere loops can compress hardware cycles from years to months, a useful blueprint for any team aiming to build software-defined hardware companies.

💰 The rise of production capital

Brett Biven’s new essay maps a new funding stack for hard-tech: R&D is still equity-financed, but the expensive middle mile, ie. the machines, tooling, first inventory, now attracts asset-backed “production capital” that looks more like project finance than venture. Brett profiles funds such as Eclipse’s Project FinCo and Industrious Ventures that write cheques against equipment collateral. Splitting tech-risk from scale-up Capex keeps dilution low for founders and lets industrial, robotics and defense founders switch on factories (hopefully) much sooner.

🏭 Production is the new product

Slodov argues the real bottleneck in today’s hardware start-ups isn’t capital or clever CAD but people who can turn designs into repeatable processes. He walks through recent examples (startups such as Humane, Kato, Saildrone) where process engineers with founder-level ownership tipped the venture from prototype to scale. The thread closes with a call for VCs to treat “production talent” as the scarcest asset on the cap-table. This fits well to what Miles (CEO Re:Build) recently shared in a call: hardware companies face two valley of death, ie. 1) from prototype to early PMF and 2) from early PMF to scaling production.

🤖 From vertical services to a self replicating robot economy

Alexander Lange from Inflection sketches how today’s vertical-AI point solutions will stack into full “physical-AI” pipelines that sense, reason and act in the real world. As visible in the graphic below, the West has a productivity issue and with that a (industrial, military and compute) sovereignty issue. He argues that the real unlock will be low-cost, self-replicating manufacturing cells that can duplicate factories as fast as software scales code. Bottlenecks remain in reliable actuators and production finance, but the prize is an economy where robots build robots and capex curves start to look like cloud compute.

📟 AI in 2027

This speculative AI roadmap is a must read for everyone. It forecasts a scenario where expert-level AI systems automating their own R&D by early 2027 and cascading to artificial super-intelligence within the same year. It details compute constraints, geopolitical race dynamics and the odds that safety research lags capability breakthroughs, then offers policy levers (think of export controls, public-compute hubs) to keep humanity in the loop. Worth reading to stress-test our own timelines for embodied AI and to see how fast upstream model progress could pull hardware demand forward.

II. Industrial Startups & Companies

🤑 Nominal has raised a $75M Series B led by Sequoia

The California start-up provides kind of a “datadog for hardware testing”: engineering teams stream live telemetry from benches, chambers, and flight tests, run hardware-in-the-loop simulations, and get automated anomaly flags in one cloud dashboard. The platform already powers Anduril, Shield AI and the U.S. Air Force, cutting test-report prep from days to minutes. Sequoia led the $75M Series B round, with Lightspeed, Lux, General Catalyst and Founders Fund participating.

🤑 AmCa has raised a $76.5M seed round by a consortium of investors

Backed by Caffeinated, Founders Fund, Lux and a16z, newly formed Advanced Manufacturing Co. of America (“AmCa”) will roll up specialised mid-tier suppliers - “the layer between standard parts and full systems.” Co-founders Jai Malik and Eli Giovanetti (ex-SpaceX ops lead) started by buying 60y-old Electro-Mech Components, whose switch gear already flies on Boeing jets. The plan is to inject modern automation, add new sensor- and power-unit lines, then scale the network as a permanent industrial platform rather than a PE flip.

🤑 Manex has raised a €8M seed round co-led by Lightspeed & Blueyard

Munich-based Manex (prev. Datagon AI) is building Qualitatio, an AI “control layer” that plugs into ERP, MES and sensor feeds to cut inspection volumes by up to 50 %. The company is already working the likes of BMW, Audi, Henkel and others on the way to automate quality management on the shopfloor. Lightspeed and BlueYard co-led the €8M seed round to accelerate Manex efforts in building Industry 5.0’s self-optimising systems.

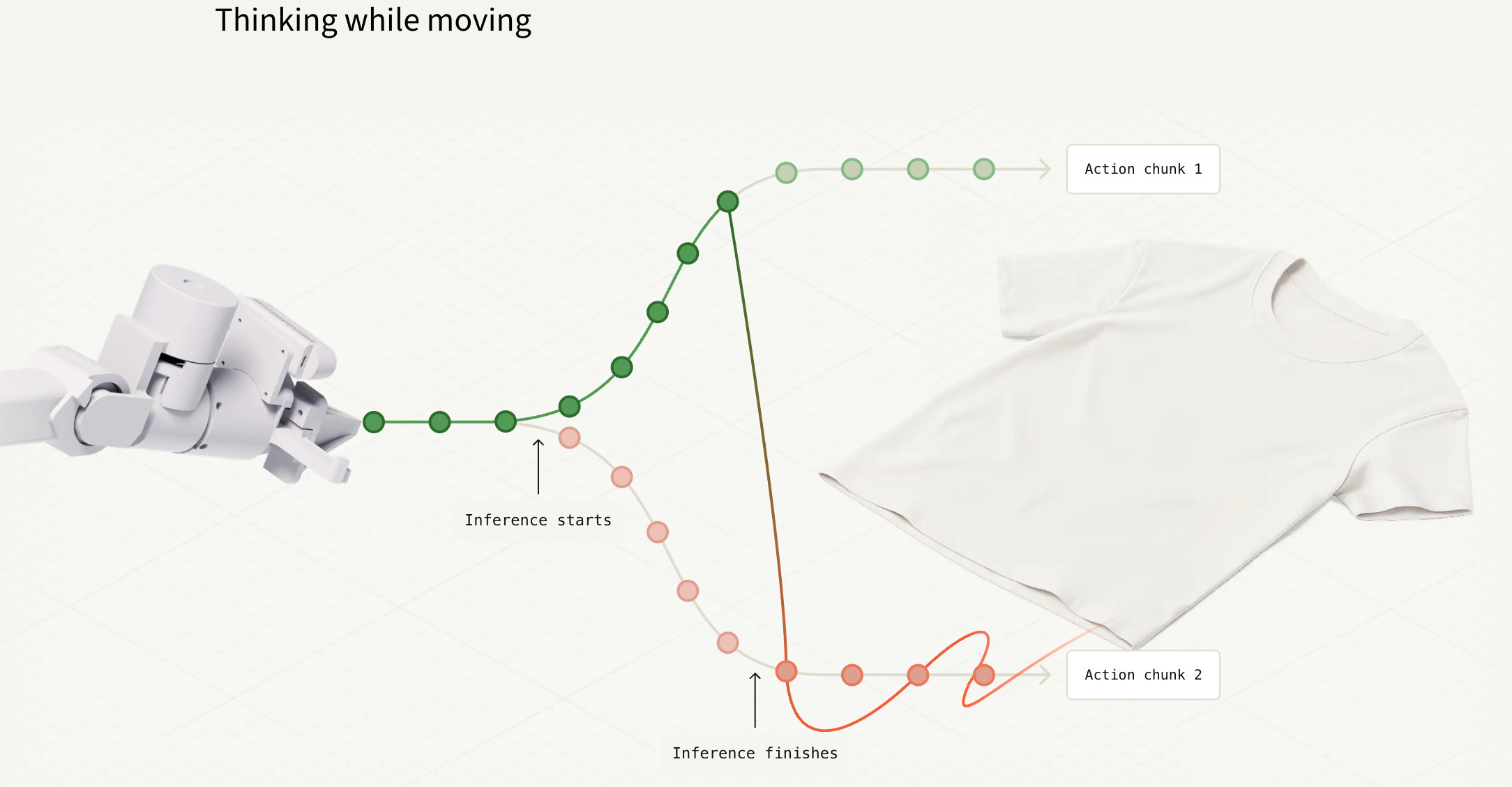

🫣 Real-Time Chunking (RTC) algorithm for robots

Controlling a robot with a huge vision-language-action model is slow; latency pauses between 1-second action chunks make arms jitter or stop. π’s new Real-Time Chunking (RTC) algorithm lets the model “think while moving”: it keeps the safe part of the current chunk, then inpaints the rest on-the-fly, like image inpainting for actions. It’s a neat, training-free trick that turns today’s large robot policies into smooth real-time controllers and useful as models grow and edge GPUs lag behind.

III. Notable funding news in short

👉 Gecko Robotics (US): has raised a $125M Series D funding led by Cox Enterprises for its infrastructure-inspecting robots. Read more…

👉 Dyna Robotics (US): has raised a $23.5M Seed round co-led by CRV and First Round Capital for its affordable, easy-to-deploy autonomous robots. Read more…

👉 Isembard (UK): has raised a $9M Seed round led by Notion Capital to reshore European manufacturing for critical industries. Read more…

👉 Emma AI (AT): has raised a €15M Seed round co-led by 3VC, Speedinvest, Serena for its AI-powered simulation technology for industrial engineering. Read more…

👉 ReRun (SWE): has raised a $17M Seed round led by P9 Capital for its open-source physical AI platform. Read more…

👉 Fabriq (FR): has raised €22M in growth capital led by Expedition Capital for its operational excellence platform. Read more…

👉 Sunrise Robotics (SI): has raised a €7.3M Seed round led by Plural for its intelligent robotic cells. Read more…

Disclaimer

Views expressed in “posts” (including podcasts, videos, newsletters, and social media) are those of the individual GC personnel who wrote the post or are quoted therein and are not the views of General Catalyst Group Management, LLC (“GC”) or its respective affiliates. GC is an investment adviser registered with the Securities and Exchange Commission. Registration as an investment adviser does not imply any special skill or training. The posts are not directed to any investors or potential investors, and do not constitute an offer to sell or a solicitation of an offer to buy any securities, cryptocurrencies, or any financial instrument or property, and may not be used or relied upon in evaluating the merits of any investment. Additional important information about GC, including Form ADV Part 2A Brochure, is available at the SEC’s website:

http://www.adviserinfo.sec.gov

Nothing here should be construed as or relied upon in any manner as investment, legal, tax, or other advice. Any projections, estimates, forecasts, targets, prospects, or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Any charts or figures provided here are for informational purposes only and should not be relied upon when making any investment decision. Certain information contained in the content has been obtained from third-party sources. While taken from sources believed to be reliable, no one has independently verified such information, and there are no representations about the enduring accuracy of the information or its appropriateness for a given situation.

To the extent any content authored or provided by any GC personnel in this forum or medium makes reference to any company in which any of the funds or vehicles advised by GC have an economic or financial interest, previous or current, none of the information provided or opinions expressed herein are connected in any way with GC’s business activities, and GC did not provide any information or assistance in the creation of this content.

Appreciate how you laid out the MES fight. It’s one of the most important but least flashy battles in manufacturing. Owning that layer is like locking in the ERP of modern industry, with higher stakes and faster cycles. I’m aiming to go into defense-industrial PM and acquisitions. Do you think the winner will be a clean-slate MES company or a point tool that claws its way up from the factory floor?