Issue #25 - The Future of Manufacturing

👋 Welcome to Issue #25 👋

Topics this time: lighthouse factories, reshoring, the industrial tech deal of the year, and many new funding rounds.

🆕 NEW POST: I just published a new blog post where I analyze and take a closer look at all the European industrial startups in my landscape. Make sure to give it a read and let me know what you think.

✋ NETWORK: I’m also spending time at the moment to better understand how manufacturing companies train their employees. If you have any insights or know somebody I could talk to, please reach out. Much appreciated!

🎥 VIDEO SUMMARY: If you don’t want to read the whole Newsletter, I recorded a quick Loom as a summary of this Newsletter.

Disclaimer: thoughts and opinions expressed in the newsletter are my own.

What I’ve enjoyed reading

#LighthouseFactories#

📈 The World Economic Forum has created a Global Lighthouse Network - a network of “advanced manufacturers that are showing leadership in applying the technologies of the Fourth Industrial Revolution to drive operational and environmental impact” how they call it. If you want to get a better picture of what that means, I recommend watching this short video where they show some factories as an example. You can also find the 40-page report from the WEF here. These are the 44 lighthouses (from January 2020):

#CovidImpact#

📝 In my last Newsletter, I wrote quite detailed about the impact of Covid-19 on the manufacturing sector. One of the take-aways was that agility and fast adoption are key to respond to the changing environment. In an age of uncertainty, Salvatore Castro from SAP emphasizes how important the coordination and collaboration between the shopfloor (“backend”) and top floor (“frontend”) is - in both ways - to ensure agility. The shopfloor needs to respond fast to changing demand and quickly bring together key stakeholders such as maintenance, operations, quality, logistics. The top floor needs to ensure to communicate efficiently changes in demand and forecasts and ensure that factory workers can work in a safe environment. All of this can work even better if factories use data insights to make better predictions and to drive continuous improvement processes.

👉 Personal opinion: Theoretically this sounds completely logical and some people might even wonder why factories haven’t been operating like this for years already. I would have liked to see some examples here of manufacturing companies that are doing this very well and some best practices they’re applying - that’s definitely missing in this article. From what I know, internal communication solutions such as Flip from Stuttgart saw a spike in demand when Covid-19 hit.

#IndustrialTechDealOfTheYear#

💡 OSIsoft is a well-known name in the manufacturing world and if you follow them you probably saw the news that the British IT company Aveva announced to acquire OSIsoft in August. John Tough from Energize Ventures even calls it “the Industrial Tech deal of the Year” on his blog. His explanation for it is very interesting, in short:

OSIsoft got started in 1980 but they raised the first round of funding in 2011 when the company did already roughly $200M in revenue. This already is extraordinary. The deal in 2011 valued OSIsoft at $450M and they raised $135M from TCV and Kleiner Perkins for a 30% stake in the business and roughly ca. 2x revenue multiple. Six years later Softbank paid a $2.9bn entry valuation which was roughly an 8x revenue multiple - great for the early investors (6x return of capital within 6 years). And now Aveva is acquiring OSIsoft that is at ca. $500M trailing 12 months revenue and a very healthy 30% EBITDA margin. Softbank will receive 1.7x return which is more than okay given the entry valuation and amount of investment.

👉 Personal opinion: As we know, good things take time and OSIsoft is not an overnight success but a success story that got started 40 years ago already. Since they have been profitable early on, they had control over their own destiny and executed impressively. I’m curious to see how the merger will play out, especially since OSIsoft has a well-known brand that Aveva might want to keep (or not?).

#Reshoring#

🏭 The fragility of global supply chains that Covid-19 has highlighted, triggered the discussion about reshoring, i.e. to move production and labor back to the home country. Especially the automotive sector with its global supply chains has suffered from supply chain disruptions with waiting times of up to several months for raw materials and parts.

This Raconteur article summarizes why a significant amount of companies considers reshoring their supply chain as you can see in the result of a survey below. The main reasons are faster adaption to changes in demand, save money by not needing additional warehouse capacities and less shipping, and air freight costs that have increased dramatically. ‘Parallel supply chains’ are an interesting concept here as well. This means companies set up multiple supply chains instead of dismantling existing global supply chains.

About industrial Startups and Companies

#FromCorporateToStartup#

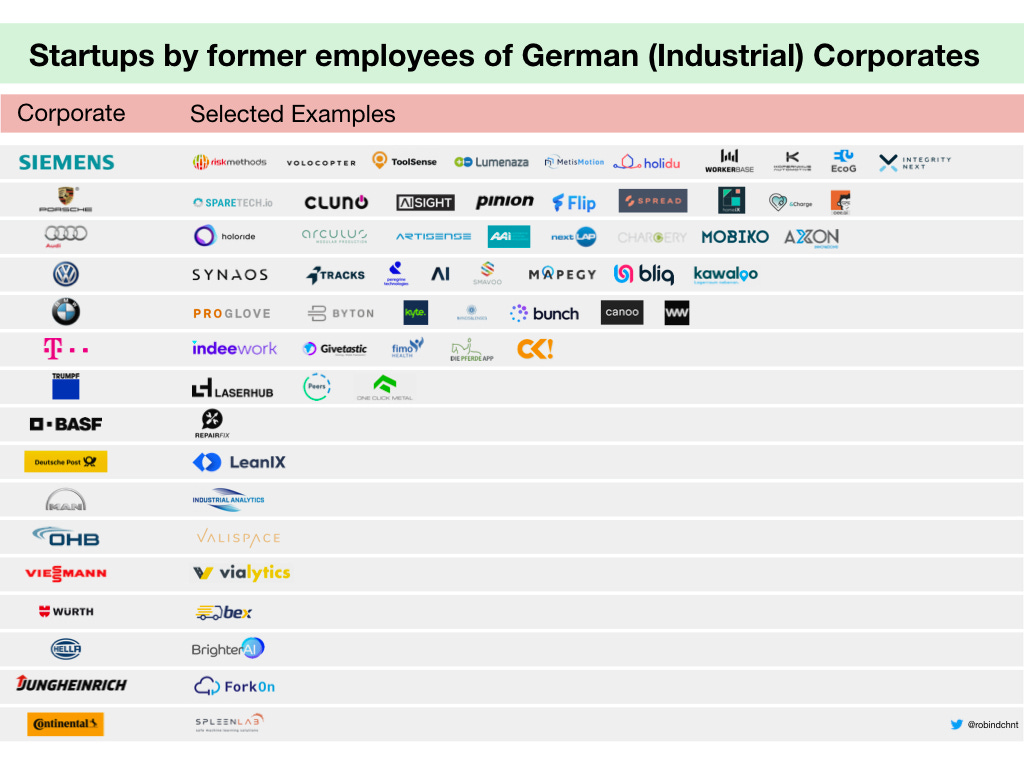

🤑 I updated my chart about Startups that got founded by former employees of German Corporates. I still focus on Industrial Corporates but since I got so much input on LinkedIn, I wanted to include all the other examples as well.

👉 Personal opinion: At the moment, Siemens is leading the list before Porsche, Audi, VW, and BMW. It’s probably not a big surprise that the big automotive players are high up on the list - also just given the total amount of employees they employ. However, I’m wondering where Mercedes Benz is? I haven’t heard of a single startup that got started by former Mercedes employees but cannot really believe that this is true. Please ping me what I’m missing here.

#Fundraising_I#

🤑 The Munich-based robotics company Magazino just announced its €21M Series C that was led by Jungheinrich AG and the European Investment Bank. It’s worth mentioning that Magazino has attracted funding from other corporates in the past including Fiege (a leading fulfillment provider) and Zalando (eCommerce).

The fresh money will be used in two ways: a) to expand international sales activities and b) to continue developing its software platform for intelligent robots that can be also used by a third party.

👉 Personal opinion: The latter is probably part of the reason for the investment by Jungheinrich. Jungheinrich is well-known for its material handling equipment, and I guess they have a high interest in using Magazino’s software to make it more intelligent.

#Fundraising_II#

🤑 I got to know Karan Talati, a former SpaceX engineer, ca. 2.5y ago because he signed up for my Newsletter and I reached out to him. He just started First Resonance together with his co-founder Neal Sarraf who has been at UpTake before. Since then we kept in touch and I’m really excited for him to finally launch First Resonance out of stealth - I’m sure it feels so good to finally share what they have been working on.

First Resonance is developing a software toolkit that helps manufacturers to coordinate their workflow processes. It helps them with production scheduling and procedures with a version control system and inventory management and material issuing solution to keep track of all the parts that are used in production. First Resonance has raised less than $2M from Fika Ventures and a few other firms. Let’s go!

#Fundraising_III#

🤑 Xometry is a name that should not be unfamiliar to you if you’re reading my Newsletter. It’s a custom manufacturing marketplace from the US that expanded to Europe last year by acquiring Shift and has just raised a Series E of $75M which brings its total funding to a whopping $193M. T. Rowe Price Associates is leading the investment together with existing investors which include Robert Bosch Venture Capital, Highland Capital, and Greenspring Associates among others.

👉 Personal opinion: I still don’t fully understand why Xometry went to Europe six years after starting in the US. The US itself is such a massive market and has so much potential that it’s a bit weird that they focused on international expansion rather than on increasing their market share in the US. As we know from other US marketplaces, it’s quite challenging to expand from the US to Europe, so I’m really curious to see how this will play out over the next years - both in the US and in Europe.

#Fundraising_IV#

🤑 Gravity Sketch announced its $3.7M seed round that we did with Point Nine together with Kindred Capital. Gravity Sketch is developing a product design and collaboration platform that utilizes virtual reality. I had my first attempt wearing a VR headset while trying to sketch a prototype together with the founder in January this year and I’m super excited for their road ahead. The unique angle here is that collaboration can take place in 3D and real-time (it’s in the cloud compared to many other design tools). If you want to learn more about it, I’ll recommend to check out this video and their homepage. That’s how it looks like if somebody is using the tool:

#IPO#

📊 The 3D printing company Desktop Metal announced in August that it plans to go public through a so-called special-purpose acquisition company (SPAC) in a deal that values the company at $2.5bn. The company has raised $438 from leading industrial companies such as BMW and Ford as well as from financial investors such as Kleiner Perkins, Lux Capital, and New Enterprise Associates. Kleiner Perkins benefits probably most from the IPO since Kleiner sits at a roughly 10x return on its full investment.

👉 Personal opinion: This IPO will be very interesting to observe since very few (industrial) startups come that far. Desktop Metal’s current revenue numbers that got shared on Twitter raise a few questions though - the current yearly revenue numbers are not that high with $26M and the growth model looks a little bit unrealistic I’d say. However, there is no official source for these numbers so we should take them with a grain of salt.

Additional thoughts on recent development

On European Industrial Startups

As mentioned in the beginning, I took a closer look at the 225 European industrial startups in my landscape and analyzed them by country, by category, by total no of employees, by money raised. What’s eye-opening is that only 7 out of the 225 companies (3.1%) were able to raise more than €50M as you can see in the chart below:

If we define ‘Series A’ as a round of at least €5M, if clearly shows you that most companies are still below the Series A mark, i.e. 183 companies (81.3%) have raised less than €5M in total. I’m sure there will be more companies that go on and raise a Series A but it definitely shows you how hard it is to scale companies in this industry.

Industrial Landscape #landscape#

There are now in total 350+ companies in the landscape and more to come soo

Again, Thanks to everybody for supporting this newsletter and for sending me interesting links. As always, any input, shares, and feedback are still warmly welcome 🙏

Robin